The global economy is struggling to get back on its feet and gasping at every step to get back into the growth trajectory. International trade plays a major role in helping the global economy stabilize and exponentially grow. In this context, exporters need measures that will boost their productions and improve their cost effectiveness to remain competitive in the global market.

The Indian Government has been looking at various avenues to provide incentives to the Industry, particularly to the exporters. Schemes like Status Holder Incentive Scrip Scheme, Star Export House Scheme, Focus Product Scheme, Market linked focus product scheme etc. source their genesis back to the fundamental idea of offsetting the Infrastructural inefficiencies that could increase the cost of exports which ultimately would put the exporters at a disadvantageous position in the global market.

With the introduction of FTP 2015–20, all the benefits provided under the erstwhile schemes mentioned above were consolidated and offered under the Merchandise Export from India Scheme (MEIS) wherein the exporters stood to gain 3% of the FOB / realised value of exported goods (whichever is lower) in the form of a freely transferrable duty credit scrip.

The Need for RoDTEP Scheme

However, In March 2018, the US had challenged various Indian Export Subsidy schemes. The dispute was heard by the WTO’s dispute resolution panel and a final report was issued on 30th September 2019.

On 31st October 2019, the WTO ruled that schemes like MEIS, EPCG, EOU & SEZ (to the extent of Duty Free Import of Capital Goods) and Duty Free Imports for Exports under the Customs Act, 1962 are inconsistent with the ASCM agreements and are prohibited export subsidies.

India has filed an appeal before the appellate forum against the ruling of WTO’s dispute settlement panel. Although, the above matter is sub-judice, the Government has decided to revisit the existing structure and roll out a scheme compatible with WTO norms. As a fallout, MEIS Scheme is being replaced by the RoDTEP scheme w.e.f. 1st January 2021.

RoDTEP Scheme : A Brief Overview

With this context, a brief overview of the RoDTEP Scheme which has replaced the MEIS scheme with effect from 1st January 2021 is summarised below :

○ RoDTEP Stands for — Remission of Duties and Taxes on Export Products

○ The scheme aims to provide a rebate of the embedded duties & taxes i.e. duties & taxes that are becoming a cost to the exporters of goods since these taxes / duties are not available as credit or refund under any other scheme.

○ For examples, duties / taxes like the Customs Duties & GST are available as refund on export of goods through various mechanisms like the AIR Duty Drawback, Brand Rate Duty Drawback, Refund of IGST on Export of Goods with / without payment of taxes.

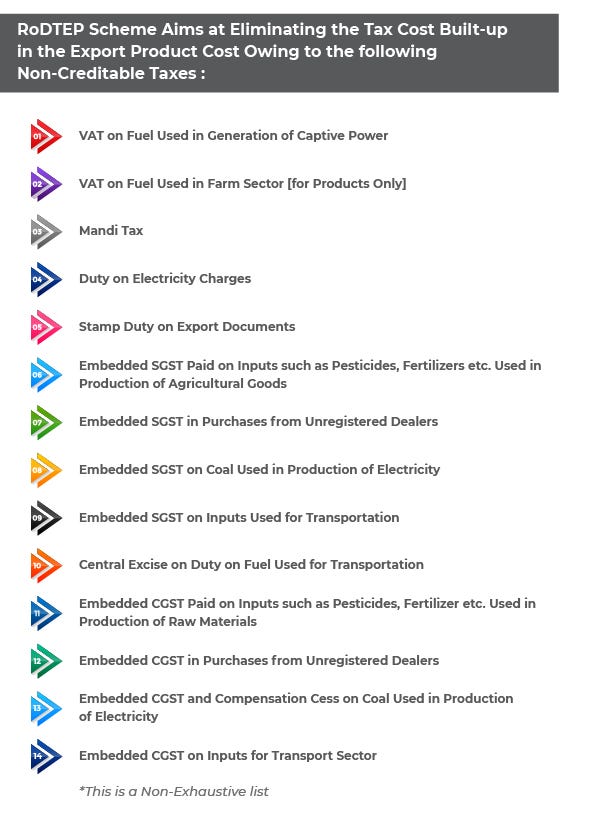

○ However, a wide array of taxes like VAT on Fuel, Additional Excise Duty on Fuel, Mandi Tax, Electricity Duty, Stamp Duty, embedded on GST on procurement of various goods not covered under GST / from Unregistered Dealers are still not available as refund / credit and hence is absorbed as a cost by exporters which ultimately get exported as a part of the Export Sale Price.

○ RoDTEP Scheme will identify such taxes / duties and provide it as a rebate to exporters in order to offset such tax cost they are currently incurring.

○ This scheme was initially announced by the Government of India (GOI) on 14 September 2019. It was to be notified from April 2020. However, GOI decided to continue to allow the benefits under MEIS up to 31 December 2020, and RoSCTL until the same is merged with RoDTEP. Therefore, the scheme is now notified w.e.f. 1st January 2021.

RoDTEP Scheme : Features & Benefits

In short, under the RoDTEP Scheme, Exporters would be granted a rebate / refund of taxes paid across the value chain of the Export Product which is not available as credit / set-off and hence is absorbed as a part of the Export Product Cost aligning with the ‘Duty Remission’ principle provided under the WTO Agreements.

The benefit would be granted by way of credit in to the electronic credit ledger of customs, calculated based on a product wise rate to be notified which would be a % of the FOB Value of goods exported based on the rates to be notified HSN wise (similar to drawback).

Having said that, we all know that the major tax incidence across the value chain of any product is GST which is available as credit (and then refund) to exporters and Customs duty is also available as refund in the form of Duty Drawback. So, what are the taxes RoDTEP Scheme would reimburse ?

First thought in our minds could be about the products that are not covered under GST. Yes, the following products are not covered under GST and hence suffer cascading effect and increased tax cost :

· Alcoholic liquor for human consumption

· Five petroleum products namely crude petroleum, high speed diesel, motor spirit or petrol, aviation turbine fuel and natural gas were presently kept out of GST. But may be brought in from a future date.

· Neither Good nor services: Sale of land or building ; Employee Employer, Court Services, Services by Legislatures, Funeral Services etc

· Goods and services exempted from GST

While some of these goods have relation with the RoDTEP Scheme, some of them are not goods and hence no relation with the RoDTEP Scheme.

Then, what are the taxes that are still alive despite implementation of GST and could GST also be a part of the RoDTEP benefit despite GST being a creditable tax ? The answer to this question is provided in the graphic below :

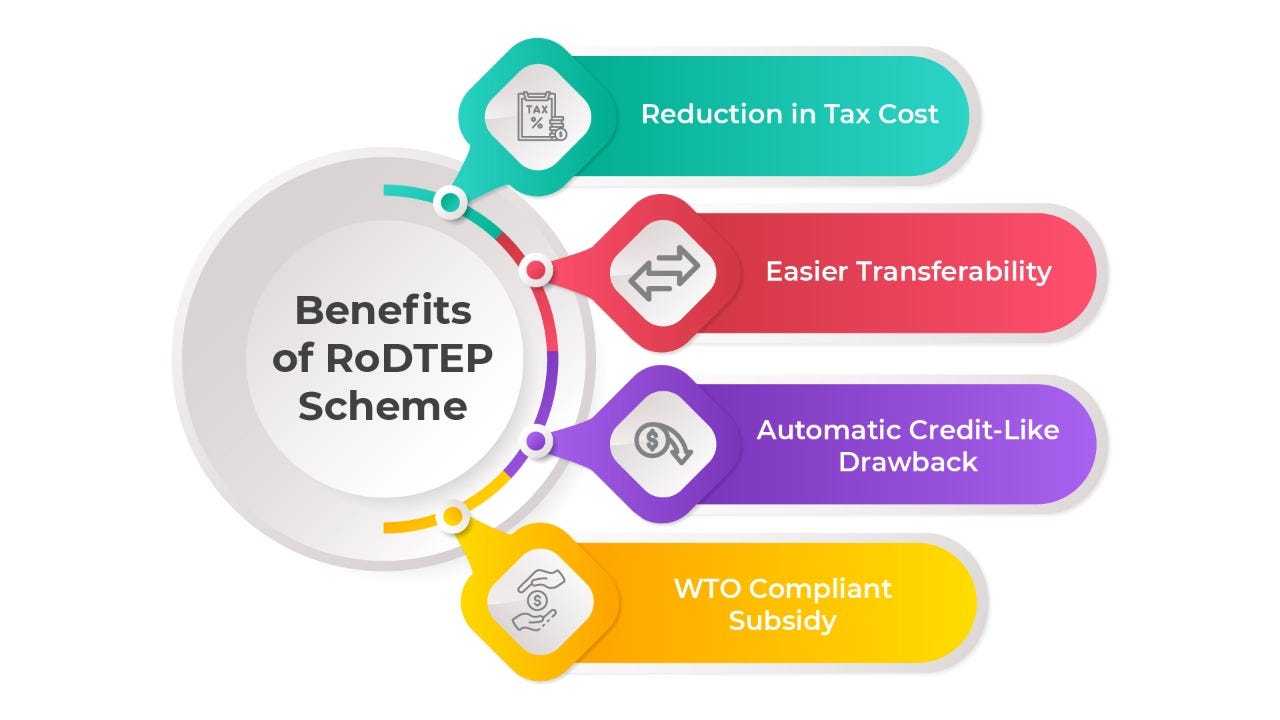

Proceeding further, let us also understand as to how the RoDTEP Scheme could be beneficial to the exporters :

- Reduction in Tax Cost

Exporters are paying these taxes and absorbing it as cost at present. With the introduction of the RoDTEP Scheme, the rebate provided under the scheme would offset such Tax Cost thereby making the product competitive in the global market. However, when it is seen as an alternative to the MEIS Scheme, it is not providing any additional / incremental monetary benefit to exporters.

- Automatic Credit like drawback

The rebate would be granted based on the declaration made in the shipping bill and a HSN wise rate to be notified like Duty Drawback. There is no requirement file any separate application like MEIS and the benefit is not granted on receipt of Foreign Currency but on Export of goods from India. This makes it a simpler way of claiming the benefit.

- WTO Compliant Subsidy

Since RoDTEP would be a WTO compliant export subsidy, there would not be any uncertainty on the benefits granted under the scheme. Moreover, this is not an Incentive Scheme that might be withdrawn at the discretion of DGFT but a duty remission scheme like drawback which is in line with the Remission of Taxes principle as per the WTO.

- Easier Transferability

The rebate would be credited to the RoDTEP Ledger of the company which can be transferred to any other importer electronically. This removes the hassles of registration of license, transferring of license etc. which will enable exporters to realize the benefit much easier.

How do exporters claim this benefit ?

Unlike MEIS Scheme, you are not required to file any separate application for claiming the RoDTEP Benefit. A simple selection & declaration in the Export Shipping bill itself would be sufficient to claim the benefit.

A concise snapshot of the procedure involved in claiming the benefit is provided below for the ready reference of the readers :

· No separate Code or Serial Number needed. RITC code given in the shipping bill will suffice.

· The declaration on the shipping bill needed to claim RODTEP :

o INFO TYPE = DTY

o INFO QFR = RDT

o INFO CODE = RODTEPY — If RoDTEP is availed ; RODTEPN — if not availed

· Additionally, for every item where RODTEPY is claimed in INFO CODE, a declaration has to be submitted in the Statement Table of the Shipping Bill

o STATEMENT TYPE = DEC

o STATEMENT CODE = RD001

Submission of the above statement code for RoDTEP availed items would indicate that the exporter has made the necessary declaration as enclosed in Annexure B, while claiming RoDTEP benefit. It is also important to note that no change in the claim can be mad after filing of EGM.

Upon filing the Shipping Bill and once the Let. Exporter Order is passed, Shipping bills are sent to Risk Management System (RMS) after EGM filed. If the SB is cleared through RMS cleared, shipping bill is queued for scroll. Else, it will come back to officer for further details. Once the officer clears the shipping bill, it will be queued for scroll.

Once the scroll is generated, the respective amounts would be available in the electronic ledger of the exporter, registered with the Icegate with their digital signature, as credit for converting into a credit scrip, provided exporter has created a RoDTEP (credit ledger) account.

While these procedures have been provided by way of an advisory by the CBIC, since the product wise rates are yet to be notified, the credit would not appear in the ledger now. However, exporters have to ensure that they provide the necessary information in the shipping bill for issuing scrolls once the rates are notified.

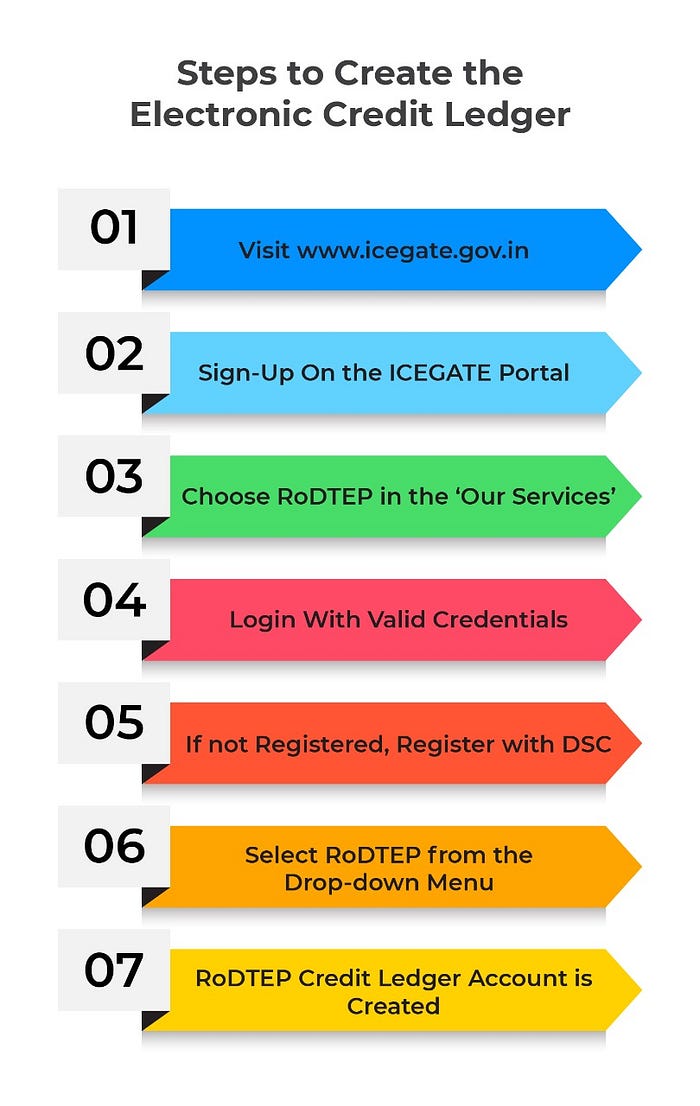

Further, one more immediate step the exporters have to take is creation of the Electronic Credit Ledger (ECL) in the ICEGATE portal. The steps to create the ECL are explained in the graphic below.

At present, facility upto creation of RoDTEP Credit Ledger Account is only opened. Once the rates are notified and detailed guidelines issues, exporters will be able to see the scroll details and by selecting the shipping bill can generate scrip which can be transacted online.

While the customs advisory also provides the mechanism of scrip transfer and other options in the portal, it is not relevant till such time RoDTEP rates are prescribed and hence we are not deep diving on to those details.

At the end of the day, RoDTEP is a duty remission scheme that could help exporters to reduce cost and hence it is imperative that they take necessary steps and implement requisite processes to ensure that the benefit is claimed.

-CA Adithya Srinivasan

(This article was first published in Sampada, the monthly magazine of MCCIA. The online edition can be accessed here https://www.mcciapune.com/media/Publication/Publication_File/Sampada_February.pdf )