MSMEs are the strongest drivers of economic development, employment, and innovation. According to the MSME Ministry’s FY19 annual report, India has 6.33 crore MSMEs out of which 99.4 percent (6.30 crore) are micro-enterprises while 0.52 percent (3.31 lakh) are medium and 0.007 percent (5000) are medium enterprises. MSMEs have a share of 31% in the nominal GDP of the country and contribute to 48% of the total exports. As per the 73rd round of National Sample Survey (NSS) conducted during the period 2015–16, the estimated employment in the MSME sector is around 11crore. Around 50 percent of the total MSMEs operate in rural areas and provide 45 percent of total employment.

MSMEs have a smaller balance sheet and hence depend acutely on cash flow from customers. In cases when the payments are delayed, MSMEs are forced to borrow to meet their working capital needs. One of the biggest challenges faced by the MSME sector is the lack of access to sufficient and timely credit. MSMEs find it difficult to obtain loans from financial institutions because of perceived higher risk, higher transaction costs, small ticket size, time-consuming documentation process, lack of awareness of the available schemes, and the limited capacity to provide immovable collateral.

According to International Finance Corporation (2018), the overall demand for both debt and equity finance by MSMEs is estimated to be Rs. 87.7 trillion which comprises Rs. 69.3 trillion of debt demand and Rs. 18.4 trillion of equity demand. Out of the overall debt demand of INR 69.3 trillion, a major part- Rs. 58.4 trillion (84%) is financed from informal sources. Formal sources cater to only Rs. 10.9 trillion (16%) of the total MSME debt financing. Within the formal financial sector, scheduled commercial banks account for nearly 81 percent of the debt supply to the MSME sector, contributing Rs. 9.4 trillion. Non-Banking Finance Companies and smaller banks such as Regional Rural Banks (RRBs), Urban Cooperative Banks (UCBs), and government financial institutions constitute the rest of the formal MSME debt flow. Within the informal financial sector, lending takes place through family, friends, money-lenders, and chit funds. As per the International Finance Corporation report the addressable credit gap in the MSME sector is estimated to be Rs. 25.8 trillion. The micro, small, and medium enterprises account for Rs.8 trillion, Rs. 16.8 trillion and Rs. 1 trillion respectively of the debt gap that is viable and can be addressed by financial institutions in the near term.

According to the RBI report (2019, the share of NBFCs in outstanding credit to MSME was 9.3% in March 2019. This trend is expected to accelerate with the emergence of FinTech (typically registered as NBFCs) focused on this segment. Share of NBFCs in outstanding credit, specifically to medium enterprises has also become significant. As of March 2018, credit from NBFCs was 17% of the total credit extended by SCBs and NBFCs to Medium enterprises.

It is important to focus on the disbursal of credit to MSMEs because the growth in credit and an increase in GDP of a nation are connected. In 2004–05 and 2007–08, India witnessed a period of high growth. The GDP of the country was around 8–9% and the demand for credit was also more. Bank credit grew 25–30% year-on-year, approximately thrice the growth in real GDP. In 2011–12 and 2012–13, credit growth reduced to 14–16%, with the fall in GDP growth. In the next 2–3 years, growth in bank credit was just around 1.3 times the GDP growth. In 2016–17, credit growth plunged to a six-decade low of 5.08 %, coinciding with the GDP declining drastically, from 8% to 7.1%. Though the GDP growth declined in the subsequent years, credit continued to grow. In 2019, bank credit grew at 14%, the highest since 2014. In 2020, the credit growth is estimated to be around 5%.

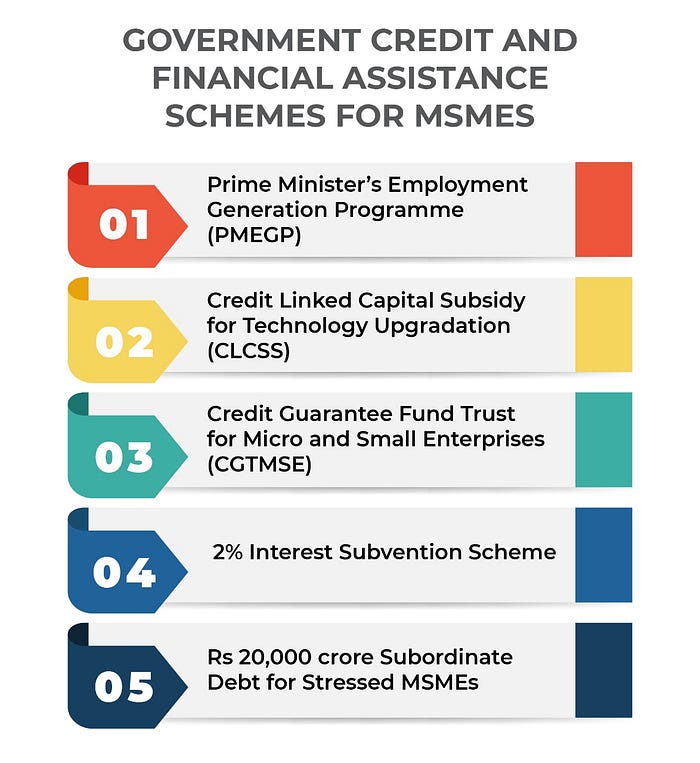

In 2020, the Covid-19 pandemic had an adverse impact on the economy. The RBI took several measures to increase the flow of credit to provide an economic stimulus. The Government of India operationalised the Credit Guarantee Scheme for Subordinate Debt for Stressed/NPA MSMEs in August 2020. Under this scheme, the government has operationalised Rs 20,000 crore stressed fund for supporting operational MSMEs which are stressed or have become NPA as on 30th April 2020. This is a part of the central government’s Rs 20.97 lakh crore Aatma Nirbhar Bharat Abhiyan. The other credit and financial assistance schemes for MSMEs are-Prime Minister’s Employment Generation Programme (PMEGP), Credit Linked Capital Subsidy for Technology Upgradation (CLCSS), and the Credit Guarantee Fund Trust for Micro and Small Enterprises (CGTMSE).

In addition to these schemes, RBI has recommended some steps to facilitate easy disbursal of credit to the MSMEs.

· Ensure uniformity in and simplification of various loan application formats and assessment processes.

· Reduce Turn Around Time (TAT) especially in the pre-LOS (Loan Origination System) or centralised sanction stage.

· Shift to a more objective appraisal system of leveraging cash flows of the unit by shifting to a Cash Flow-based lending (CFL) appraisal system from traditional balance sheet-based funding.

One of the ways to fill the credit gap is using supply chain financing or reverse factoring. SCF is a modern tech-based method that focuses on optimizing cash flows. SCF is a win-win solution for both the buyer and the supplier because it gives early access to funds for the sellers and buyers can avail themselves a longer time before making payment. SCF is initiated by the ordering party to ensure its suppliers are able to finance the receivables more easily and at a lower interest rate than what would normally be offered. The Government of India has introduced the Trade Receivables Discounting System (TReDS) to give a boost to SCF. The platform gives MSMEs access to a large number of financiers who are willing to place bids on their invoices. One of the biggest advantages of the TReDS platform for MSMEs is the fact that the funds disbursed through TReDS are without recourse or collateral. Since 2017, TReDS has processed over Rs 24,000 crore worth of invoices that helped over 14,000 MSMEs with better liquidity and access to funds. The RBI has also launched the Account Aggregator (AA) Framework. The AAs are RBI licensed financial entities that will bring the financial data of customers on a single platform. This data would be shared with lenders upon the consent of the users. It will make the process of availing loans much easier because the paperwork and processing time would be reduced. The government has also announced the Open Credit Enablement Network (OCEN), a new credit protocol infrastructure to work with the AAs. OCEN will provide the foundation for the emergence of a credit market place. It will act as a link between lenders and marketplaces and enable them to utilise and create innovative, financial credit products at scale.

It is the need of the hour to democratize credit. Ensuring disbursal of credit to the MSME sector would not only help it to grow but would empower us to unlock our complete economic potential.

Source: MSME Ministry Report(2019), International Finance Corporation Report(2018),RBI Report(2019)

-Sanika Tapre

(Sanika is a Youth Fellow at MCCIA.)